A year ago I wrote that Canada produces incredible founders and loses the best of them before a local VC ever sees them, pulled south by US firms offering better capital, networks, and belonging. A year on, with better data, it’s worth revisiting — because the numbers let me show the machine far more precisely this time: how it works, who it takes, and what it has already built.

When a Canadian founder builds a giant company in the US, that’s a Canadian win. Claim it. They’re proof of what Canada produces, building at the highest level. They just went south to do it. It isn’t a failure. It’s an opportunity we keep missing, and one we don’t have to.

Canada hands these builders to non-profits: incubators, accelerators, grants, built to help, never to own. The Americans do similar support, but they treat it as investment, not charity. That difference compounds. It funds a sophisticated system that targets Canadian and American builders as early as high school, and they place Canadians into it deliberately, because the returns are there. This is how they do it.

It’s a conveyor belt, not a few accelerators

The mistake is picturing this as a few famous accelerators skimming finished founders off the top. It isn’t. Over the last five to ten years, US investors have built a program for every stage of a technical person’s path — and crucially, each one is engineered to remove a specific reason someone might have stayed put. Walk the ladder:

| Life stage | US programs targeting it | The friction it removes |

|---|---|---|

| High school / pre-college | Z Fellows (takes high schoolers), Thiel Fellowship, 1517 Fund | The belief that you need a degree — or permission — before you’re allowed to build |

| In college | Neo Scholars, Pear Dorm, Contrary, Emergent Ventures, YC’s apply-and-defer | Having to choose between staying in school and starting |

| New grad / pre-idea (−1 to 0) | Founders Inc, The Residency, SPC Fellowship | Needing a finished idea, a co-founder, or a team before you can begin |

| First-time founder with a thing | Y Combinator, PearX, a16z Speedrun | Capital scarcity — and, via Speedrun, the visa itself |

| Repeat / proven founder | HF0 | Every life logistic, so you do nothing but build |

The full version of this ladder — every California program filling in each rung, with terms, locations and cohort dates — is laid out in the companion reference: The Founder Friction Ladder.

Look at what that table means. A talented kid in Waterloo or Markham can now be inside a US-funded program before they finish high school, get a $10K Z Fellows check to spend a week building, take a Neo Scholars grant to try a startup for a semester without dropping out, move into a Residency house the summer after graduation, raise $500K from YC, take $1M and a visa from a16z, and — if it works — get pulled into HF0’s mansion for the next one. At no point in that decade does the conveyor hand them back. There is always a next rung, and it is always in San Francisco.

A few of the rungs, concretely:

- —Z Fellows — Cory Levy’s one-week program. $10K, optional, at a $1B cap (functionally free), or no equity if you decline. Takes high schoolers. Levy has reportedly put close to 20% of his fund into teenagers. The pitch is don’t drop out, just simulate being a founder for a week.

- —Neo Scholars — Ali Partovi’s. A $20–25K equity-free grant for ~30 college students a year, plus a “Semester in SF” building at Neo’s studio with private Q&As with the likes of Sam Altman and Satya Nadella. Forbes called it harder to get into than Harvard. Neo wrote the first check into Cursor.

- —1517 Fund and the Thiel Fellowship — the originals. Thiel pays young people to leave school; 1517, run by its co-founders, backs students and dropouts and is explicit that they get to these people “long before they know they should apply to anything.”

- —Contrary funds students in Canada — a small early check as a relationship tool, on the cap table before any domestic fund shows up. Emergent Ventures grants do the same with no relocation required (a dozen-plus Waterloo students held them when I last wrote about this). Buildspace was the magnet for this whole cohort before it folded; its model is what The Residency and Founders Inc run now.

- —The Residency — young builders in ~a dozen houses worldwide, ~five in SF. Its own framing: it exists to let investors observe founders over time. Talent identification dressed as co-living.

- —Founders Inc — a 42,000 sq ft Fort Mason campus, hardware lab, first checks of $100–250K. “The place builders go to become founders.” A belonging machine first, a fund second. Its Off Season is the rung built for exactly this drain: six weeks each summer at the SF campus for ~100 students, recent grads, and dropouts — no curriculum, up to $250K to the top teams — pitched explicitly as the alternative to a summer internship. Last summer’s teams went on to YC and Speedrun.

- —YC, PearX, a16z Speedrun — the well-known top of the funnel. YC’s $500K and ~1% acceptance; PearX’s $250K–$2M plus a recruiter who hires your founding team for you; Speedrun’s up-to-$1M, ~$5M in credits, and a Global Founders Program that handles your visa.

And the rungs above are a sample, not the map. This is only the layer you can see — it doesn’t begin to count the quieter, more sophisticated talent identification the savviest US firms do off the books: the funds that know exactly the kind of person they’re looking for and reach the right nineteen-year-old through a warm introduction years before any program posts a deadline. For every program with a website there’s another relationship that never had to advertise. The visible conveyor is the floor, not the ceiling.

That’s the depth. Now the results.

What the conveyor produces

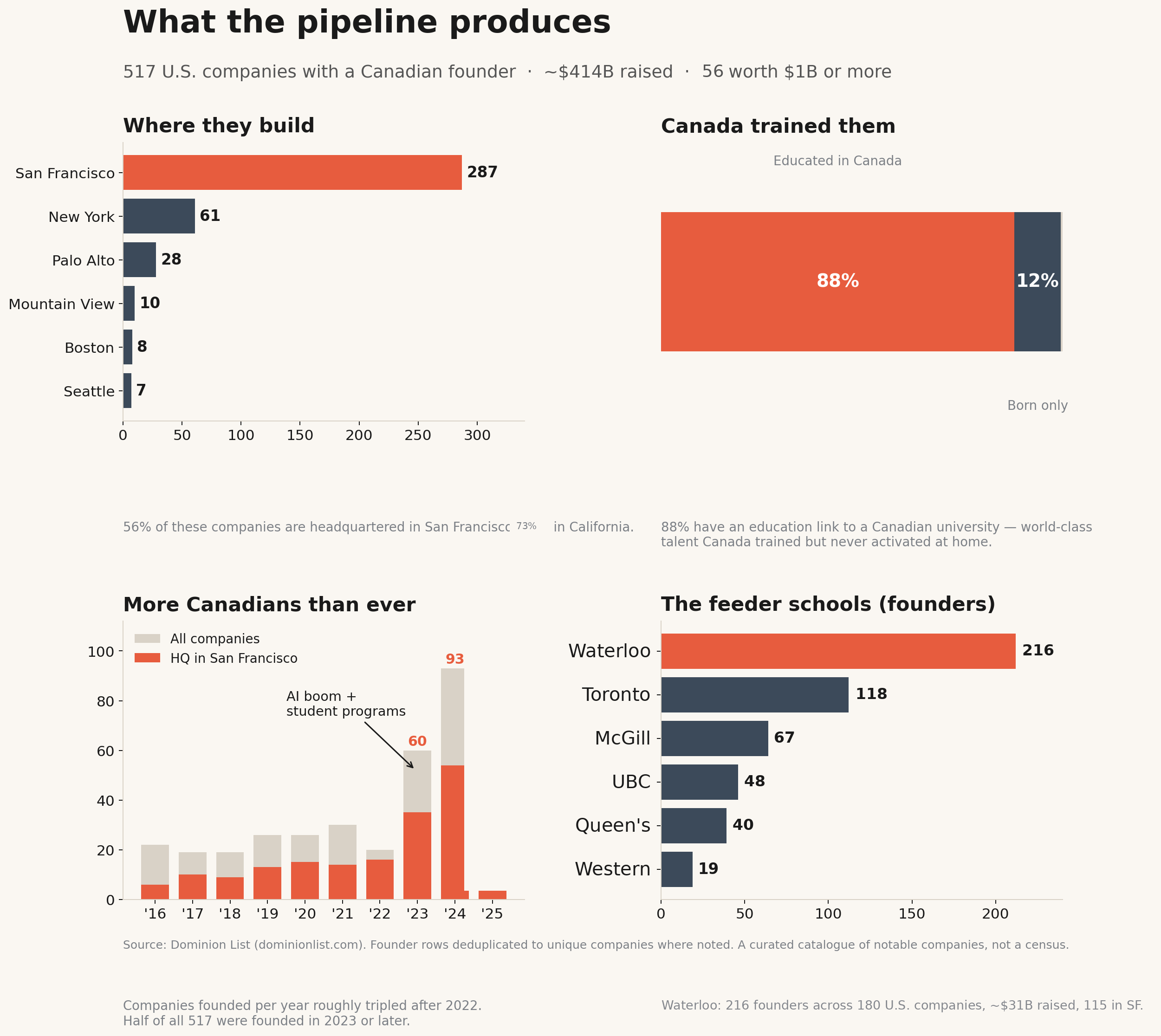

Dominion List is a running catalogue of US companies founded by people with a Canadian connection. It’s a curated list of notable companies, not a census — so treat it as a portrait, not a population count. But as a portrait of where Canadian-made talent ends up, it’s damning.

Deduplicated to unique companies, the list currently holds 517 US-based companies with a Canadian founder. Together they’ve raised about $414B. Fifty-six are worth $1B or more on disclosed valuations; nineteen are public; fifty-nine have been acquired. Few of these are cute side projects that left town. Together they make up a meaningful share of the last decade’s most valuable American technology companies — staffed, in part, by people Canada educated.

This is talent we trained and then never activated. Sort by how these founders are Canadian and the answer is overwhelming: 88% have an education link to a Canadian university. Only about 12% are birthplace-only. The line runs straight out of our lecture halls — world-class ability we built, then failed to raise to its potential, so it went where it was embraced. This is a pipeline, not nostalgia about people who left as children.

| Connection to Canada | Share of founder links |

|---|---|

| Educated here (incl. born + educated) | 88% |

| Born here only | 12% |

They nearly all end up in one place. 73% of these companies are headquartered in California; 56% in San Francisco alone. New York is a distant second at ~12%. The conveyor has one destination.

The feeder schools are exactly who you’d expect:

| University | Founders | Companies | HQ’d in SF |

|---|---|---|---|

| University of Waterloo | 216 | 180 | 115 |

| University of Toronto | 118 | 107 | 59 |

| McGill University | 67 | 59 | 30 |

| University of British Columbia | 48 | 41 | 22 |

| Queen’s University | 40 | 33 | 13 |

| Western University | 19 | 18 | 13 |

Waterloo is the volume story: 216 founders across 180 US companies, roughly $31B raised, 115 of them in San Francisco. Toronto is the frontier story — its enormous capital footprint concentrates in a handful of generational companies rather than spreading across hundreds of startups. Which brings us to the part that should end the debate:

The crown jewels of the AI era carry Canadian-trained founders. OpenAI, Anthropic, and xAI — the three leading frontier labs, north of $300B in combined funding — all appear on this list through founders and early scientists trained in Canada, the lineage that traces back to Geoffrey Hinton’s lab at Toronto. Add Uber and Databricks and you have a sense of the altitude. These are American companies. The talent inside them is, substantially, ours.

| Company | Capital raised | Canadian-trained founder(s) |

|---|---|---|

| OpenAI | ~$168B | Ilya Sutskever & Andrej Karpathy (U of Toronto) |

| Anthropic | ~$124B | Chris Olah (co-founder; born in Toronto) |

| xAI | ~$42B | Yuhuai Wu & Guodong Zhang (U of Toronto) |

| Uber | ~$15B | Garrett Camp (University of Calgary) |

| Databricks | ~$14B | Matei Zaharia (Waterloo), Reynold Xin (Toronto) |

(A “link” means a founder studied, trained, or was born in Canada — not that the company is Canadian. That’s the point: the value accrued elsewhere.)

And it’s accelerating. From 2016 to 2022, this list added 20 to 30 Canadian-founded US companies a year. Then it inflected: 60 in 2023, 93 in 2024, 87 in 2025 — the annual rate roughly tripled, and half of all 517 companies were founded in 2023 or later. The share landing in San Francisco climbed right along with it (about two-thirds of the 2025 cohort). Some of that steepness is a curated list catching recent names more easily than old ones — but a threefold jump that lines up exactly with the AI boom and the explosion of student-stage programs is not an artifact. None of this is history you can shrug off — the conveyor is pulling more Canadians than ever, and the people it’s processing now were in a Canadian classroom eighteen months ago.

Why YC’s slip-up matters

Here’s the bow on it. In late January 2026, Y Combinator quietly removed Canada from its approved incorporation jurisdictions, which would have forced Canadian teams to flip to Delaware to take the $500K. After a week of backlash, Garry Tan reversed it and reassured everyone that YC funds dozens of Canadian startups a year.

But read why he said they pulled it: YC’s top-performing Canadian companies all reincorporate in the US anyway — and over YC’s twenty-year history, the ones that flipped reached roughly twice the average valuation of those that stayed incorporated in Canada.

That’s the Dominion data in YC’s own words. The policy got reversed; the belief behind it is just true. YC briefly made the structural reality explicit, the community made them take it back, and the reality kept operating underneath — because it’s the same reality this dataset describes. The drain doesn’t need a policy. It’s already built into where the capital, the density, and the upside live.

What they all sell — and what Canada doesn’t

Strip the branding off every rung of the conveyor and they offer the same three things, and it’s exactly the package Canada underdelivers:

- Capital at the idea stage — or before there’s an idea at all. Canadian institutions, by founders’ own accounts, won’t move until success is already obvious. By then the founder is gone.

- Density — a room of people going all-in, which matters more than any curriculum. Co-living, campuses, retreats: peer pressure as a service.

- Access — mentors, a Demo Day with a thousand checkbooks, a recruiter who staffs your team, a Q&A with the CEO of OpenAI.

The newest move across all of them is friction removal. Speedrun does your visa. Pear does your hiring. Neo and Z Fellows say you don’t even have to drop out. Each one quietly absorbs a reason a Canadian might have stayed. The salary gap — US tech pay runs ~46% higher adjusted, roughly USD $122,600 vs CAD $83,700 — is just the backdrop. They aren’t winning on salary. They’re winning on speed, belonging, and the removal of every excuse. And they now start the pitch while the target is in second year of undergrad. Or earlier.

The opening hiding in plain sight

Look at the conveyor again. YC, Speedrun, PearX, HF0, The Residency, Founders Inc, Neo, Z Fellows. Notice how alike they’ve become — twelve weeks, small batch, SF, a retreat to open and a Demo Day to close, $X for Y% on a SAFE. They are converging on one playbook, run faster and with better catering each cycle.

When everyone runs the same funnel, the funnel stops conferring an edge. So the answer for Canada was never “build our own YC.” A Canadian YC-clone arrives a year late to a strategy that’s already commoditizing.

The thing Canada has is the one input none of these programs can manufacture: the builders. The Dominion data proves it — 88% of those founders are our graduates. Waterloo produces them on a schedule. The missing piece isn’t talent, or even capital — it’s the infrastructure to recognize and back people before someone in San Francisco does, and now “before” means before they’ve finished a degree.

Pride doesn’t compound, though — and that’s the catch we keep ignoring. The success is Canadian; the value capture is American: the jobs, the equity, the secondary founders each exit spins out, the angel checks those founders go on to write, the tax base, the next fund.

All of it pools in San Francisco. We trained the talent and handed it off at the exact moment it became investable, because our half of the system runs on charity and theirs runs on capital. That gap — charity here, investment there — is a massive, ongoing transfer. We pay; they earn.

That’s the real lesson of the drain — and there’s no single solution to a gap this wide. No one accelerator, no one fund, no one policy closes it; this was never a problem you solve once. We keep missing the opportunity because we keep filing it under charity: incubators, grants, help, built to assist and never to own. But it was always an investment, and the Americans have been collecting the returns for a decade.

So we’re doing the other thing, in Waterloo. Builders Club is the density — a community of builders going all-in around each other. Barn Ventures is the capital that shows up before it makes sense: first cheque, pre-incorporation, equity early, while the founder is still in the room and not yet on a flight to San Francisco. We’re not trying to replace the conveyor — you can’t out-San-Francisco San Francisco, and some of the best will still go. We’re getting in at the earliest stage: the same three things it sells — capital, density, access — offered first, at home, as investment. A stake in the talent we already produce, instead of a free handoff.

Waterloo produces the talent on a schedule. The opening is to back it here, as if it were worth owning — because it is. Right now we’re running someone else’s playbook a decade behind. The way out was never to run it better. It was to run a different one — on the one input no program can manufacture: the builders, and the place that keeps making them.